Courtesy of iii.org

The 2020 Atlantic hurricane season activity is projected to be “extremely active,” according to Triple-I non-resident scholar Dr. Phil Klotzbach.

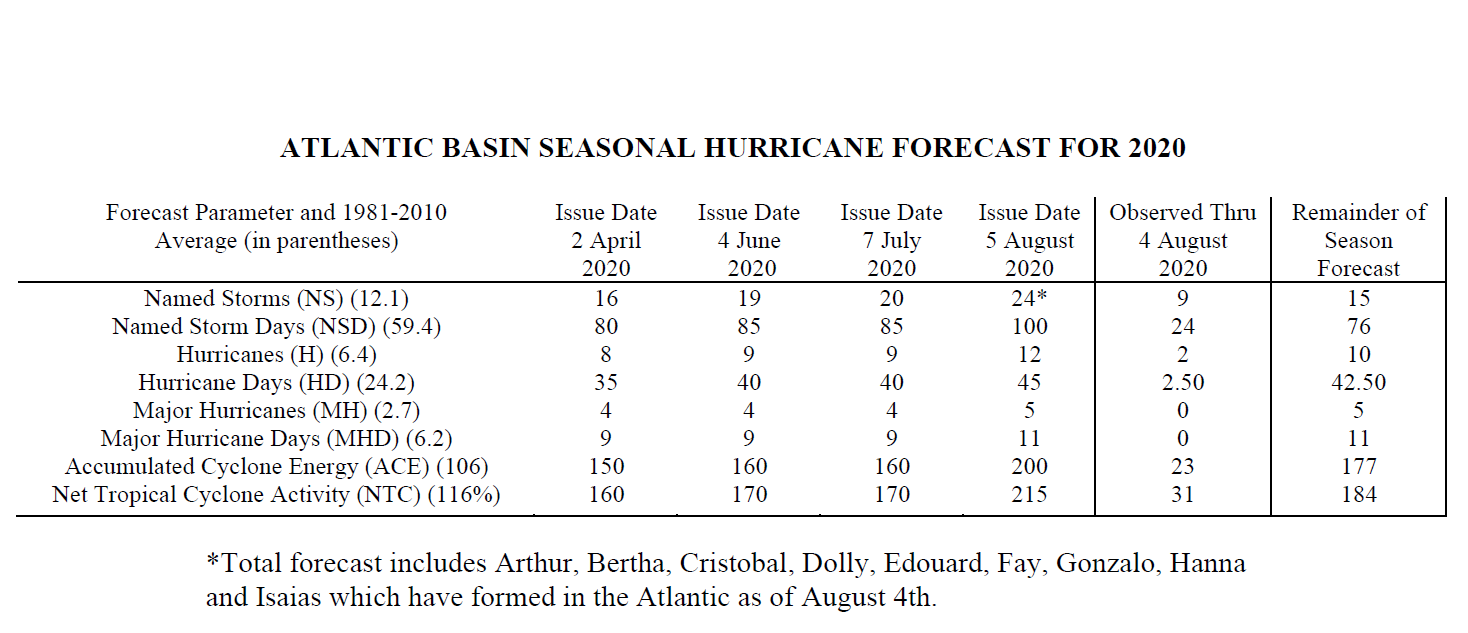

Dr. Klotzbach, an atmospheric scientist at Colorado State University (CSU), and his team issued an updated forecast on August 5. They project the 2020 Atlantic hurricane season will have 24 named storms (up from 20 in the previous forecast), 12 hurricanes (up from nine), and five major hurricanes (up from four).

The 24 named storms include the storms that have already formed. An average season has 12 named storms, six hurricanes and three major hurricanes.

The activity is driven in part by reduced vertical wind shear. Strong wind shear tears apart hurricanes. Observed wind shear has been very low in July, which means it’s also expected to be low at the peak of the season from August to October.

The probabilities of U.S. hurricane landfalls are also elevated simply because we are expecting more Atlantic storms. The U.S. has already experienced two landfalls this season with Hanna and Isaias.

People in hurricane-prone areas are advised to have a plan in place and follow the directions of local emergency managers if storms threaten.